If you do not pay real estate tax, the federal government will have a claim on a few of the house's worth. That can make things complicated. Home loan loan providers frequently make buyers who don't make a 20% deposit pay for private home mortgage insurance (PMI). This is insurance that assists the bank get its money if you can't afford to pay.

If you can avoid PMI, do so. It can be tough to get a lender to remove it even if you have 20% equity. There's no guideline stating they need to and sometimes they will just if a new appraisal (an included cost to you) reveals that you've hit that mark.

The last cost to think about is closing costs. These are a selection of taxes, costs, and other assorted payments. Your home mortgage lender need to offer you with a good-faith estimate of what your closing expenses will be. It's a price quote due to the fact that costs alter based on when you close. Once you find a house and start negotiating to acquire it, you can ask the current owner about residential or commercial property taxes, utility costs, and any property owners association charges.

4 Simple Techniques For How Do Mortgages Work For Custom Houses

But it is very important to learn as much as you can about the genuine expense of owning the home. Once you have a sense of your individual financial resources, you need to understand just how much you can afford to invest. At that point, it might be time to get a preapproval from a home loan loan provider.

This isn't a real approval, though it's still essential. It's not as excellent as being a money purchaser, but it reveals sellers that you have a great chance of being approved. You don't need to use the home loan company that offered you a preapproval for your loan. This is simply a tool to make any offers you make more appealing to sellers.

Being the greatest offer helps, however that's not the only aspect a seller thinks about. The seller also wishes to be confident that you'll be able to get a loan and close the sale. A preapproval isn't a warranty of that, but it does suggest it's more most likely. If you have a preapproval and someone else making a deal doesn't, you may have your offer accepted over theirs.

The Basic Principles Of How Does Securitization Of Mortgages Work

Since of that, don't automatically choose the bank you have your checking account at or the lender your property representative suggests. Get several offers and see which lending institution offers the very best rate, terms, and closing expenses. The easiest method to do that is to utilize an online service that revives several offers or to use a broker who does the same.

If you have problems in your mortgage application-- like a low credit score or a very little deposit-- a broker might assist you discover a considerate bank. In those cases, you may also want to speak with cooperative credit union, specifically if you have actually been a long-term member of one.

An excellent home mortgage broker must be able to discover if you get approved for any federal government programs and discuss to you which kind of home loan is best for you. The last piece of the mortgage loan procedure is the home itself. how do reverse mortgages work in california. Your loan provider can't authorize a loan without understanding the information of your home you plan to buy.

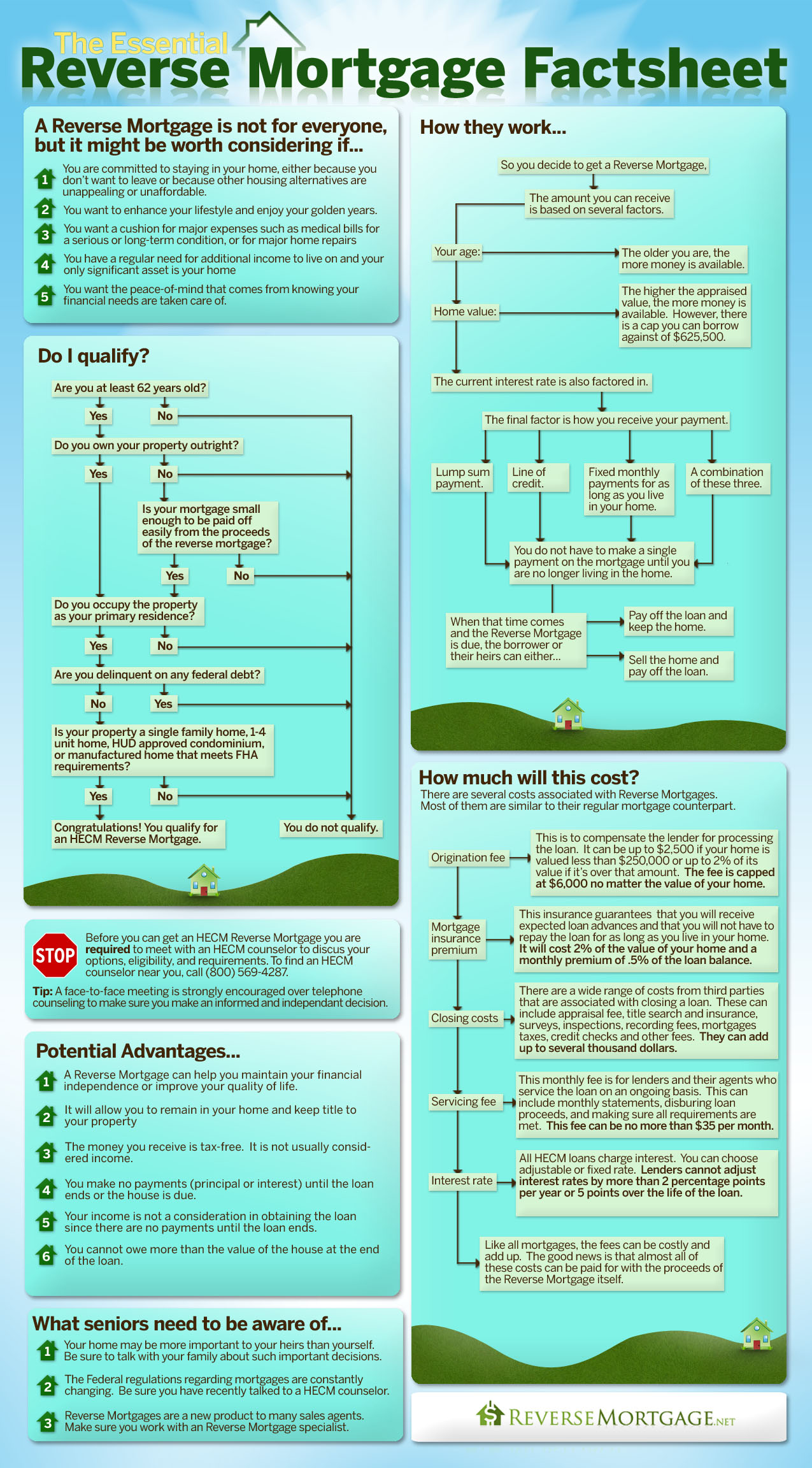

Not known Facts About How Do Reverse Mortgages Work?

This is where you'll need all of the documentation discussed above. You'll require your most-recent pay stubs. Let your employer understand that your potential lending institution might call the business to confirm your work, too. The home mortgage lender will likewise purchase an appraisal. An appraisal sets the worth for the home in the eyes of the mortgage loan provider.

The crucial factor is the worth the appraiser appoints. In current years, appraisals have actually gotten more downhearted. Lenders don't wish to loan you money they can't recover, so if the appraisal values the home below what you're paying, your lender may desire a bigger deposit. On top of the appraisal, you'll likewise have a home inspection.

In most cases, you'll hire an inspector (though your lending institution or property agent can suggest one). Find somebody with good reviews and accompany them while they check the property. A great inspector will see things you don't. Maybe they see signs of past water damage or believe the roofing system needs to be fixed.

The Greatest Guide To How Do Buy To Rent Mortgages Work

Do the exact same with the showers and tubs. Flush all the toilets. Make sure any consisted of home appliances work. Inspect to see that doors close and lock appropriately. Make sure that the garage door opens as it should. That's not an extensive list, and the inspector may examine some of those things.

If minor things are incorrect, you may have the ability to get the existing owner to fix them. When something significant appears, your mortgage loan provider may insist that modifications are made or that the cost is decreased. You're not looking to be a jerk here. The goal is to determine things that are genuinely wrong and address them.

Assuming you discover a house and get it assessed and examined, it's time to close the loan. When you've discovered a home, placed it under agreement, and received a mortgage dedication-- a guarantee to provide you the cash-- from your loan provider, it's time to close the loan. However there are a few things you need to do first.

The Best Guide To How Do Second Mortgages Work In Ontario

Ensure any needed repair work were completed and that no brand-new damage was done during the relocation. It's not fun to ask for compensation for damage or incomplete repairs at closing, however you ought to if something's wrong. Before the closing, check in with your loan provider to make certain you have everything that's required with you.

It's likewise really essential to check out the closing declaration. Your property representative can explain where it's various from the quote and why. In a lot of cases, you'll pay interest on the loan based on the number of days left in the month and you may have some other full or prorated charges.

Do not open a new charge card, buy an automobile, or spend a considerable amount of money. You do not want your credit history to fall or your loan provider to change its mind at the last minute. When you close your home mortgage loan-- which generally includes a great deal of signatures-- it's time to take a minute to praise yourself.

Not known Facts About How Do Muslim Mortgages Work

That is worthy of a bit of celebration-- even if you still deal with the difficulties of moving into and getting settled in your new house. how do fixed rate mortgages work.

We developed LendGo as an online platform where banks complete for debtors. Whether you're re-financing your home loan or contrast shopping for a home purchase loan, LendGo is here to help you protect the lowest rates and closing costs possible. 2017 All Right Scheduled.

When you take out a home mortgage, your loan provider is paying you a large loan that you utilize to acquire a home. Due to the fact that of the danger it's taking on to release you the home mortgage, the lending institution likewise charges interest, which you'll need to pay back in addition to the home mortgage. Interest is determined as a percentage of the home mortgage quantity.